Strata Market Update: July 2026

Key takeaways

- The market is softening, but not evenly.

- Better buildings are attracting better insurance.

- Underwriters are looking beyond claims history to building quality and governance.

- Transparency is becoming a competitive advantage.

- The gap between well-managed and poorly managed buildings is widening.

Market Overview

After several years of steep premium increases, the Australian strata insurance market is softening. The hard market cycle, characterised by significant premium hikes, reduced insurer competition, and tighter underwriting has to an extent reduced.

For well-maintained buildings with clean claims histories, the second half of 2026 is shaping up to be the most favourable renewal environment since 2021.

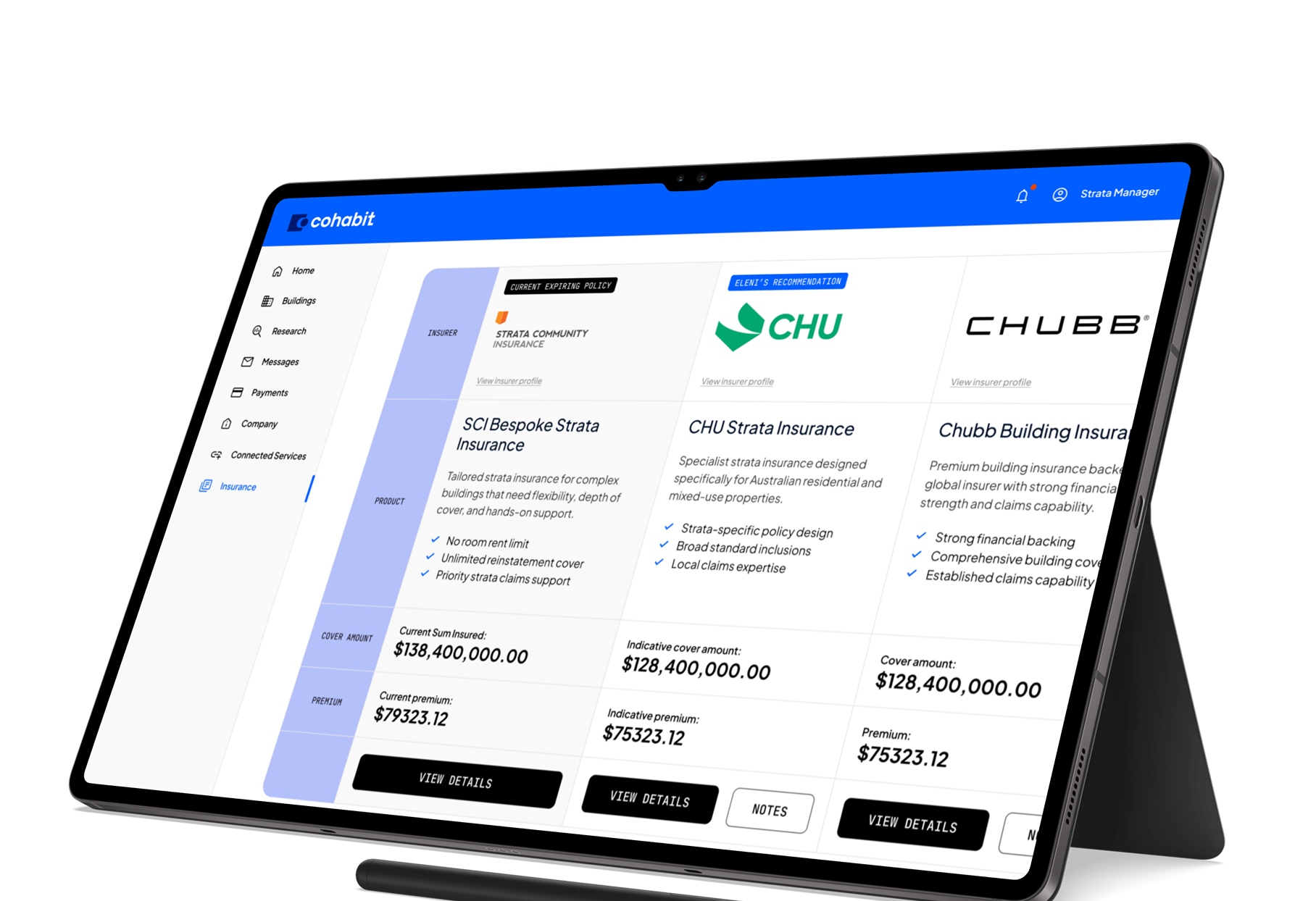

The market is increasingly divided. Buildings that present well are attracting genuine competition and, in some cases, meaningful premium reductions. High-risk or poorly maintained schemes continue to face limited insurer appetite and elevated pricing. Where your building sits in this divide is not just a 2026 concern, it is one of the strongest predictors of insurance outcomes over the years ahead.

Competition among existing strata underwriters has intensified, with new market entrants anticipated shortly. This additional capacity is expected to put further downward pressure on premiums for lower-risk properties and create more choice for owners corporations currently limited to one or two quotes.

Insurers are also broadening their policy wordings to reflect the evolving strata landscape, notably, cyber coverage is being introduced in response to increasing social engineering fraud targeting strata schemes and owners corporations.

At the same time, a number of agencies have significantly increased their single-risk capacity, with some doubling their limits and appetite. This should give larger buildings greater flexibility across both co-insurance arrangements and single-insurer structures.

Looking into the second half of 2026, the trajectory is positive for well-maintained risks. Underwriters have signalled that buildings with near-clean claims records can expect consistency at renewal and, in some cases, competitive discounts as insurers work to retain and win business.

Premium Composition

Understanding where your premium goes provides important context:

- Base Premium - 61% Comprises 47% for claims and reinsurance (directly tied to your building's risk profile and history) and 14% for underwriter overhead and administration costs.

- Brokerage Fee - 15% The cost of distribution, which varies depending on the broker used.

- Emergency Services Levy - 9% A government charge applicable in NSW only.

- GST - 8% Government charge.

- Stamp Duty - 7% Government charge.

Nearly half of every premium dollar goes toward claims and reinsurance costs. This is why a building's claims history, maintenance standards, and exposure to natural hazard risk carry such weight in determining what is paid.

Underwriting Evolution

Strata insurance underwriting is undergoing a significant shift. Risk modelling has evolved to incorporate flood zones, cyclone corridors, and bushfire overlays. Beyond physical risk, committee and strata manager behaviour is emerging as a rising underwriting factor, how a scheme is actually managed, and whether that management reduces or amplifies claims risk, is now an active consideration when broking.

Insurers are evaluating the following factors:

- Claims history: the most direct signal of a building's risk profile.

- Outstanding defects: how long they have been present, their nature (life safety versus cosmetic), and the proactivity of owners in addressing them.

- Maintenance records: upkeep of roofs, gutters, plumbing, and common property.

- Building-specific risks: the presence of ACP/EPS cladding, lithium-ion batteries, or high-risk commercial tenants.

- Sum insured: whether valuations are current and sufficient to avoid gaps in coverage or underwriting scrutiny at renewal.

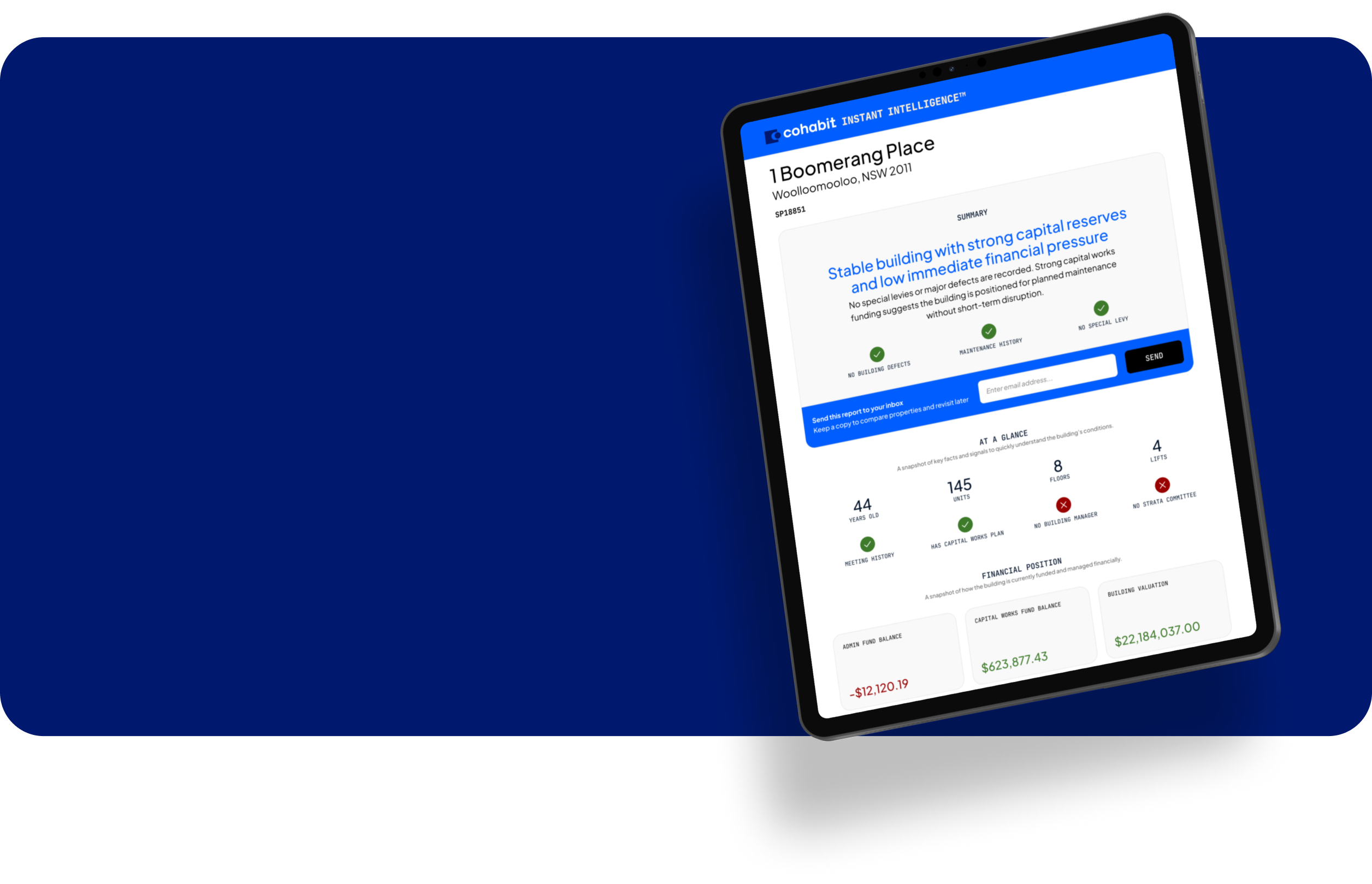

Schemes that actively manage their buildings, maintaining roofs, clearing gutters, ensuring fire compliance, and keeping documentation current, are increasingly rewarded with better premium outcomes. Proactive management produces resilient buildings, and resilient buildings attract better insurance terms.

Building Defects

Building defects, particularly waterproofing failures, structural issues, and combustible cladding, remain a significant underwriting concern. A NSW Strata Defects Survey conducted in 2025 found that 53% of buildings surveyed had serious defects in common property, up sharply from 39% in 2021. Legal precedents established over the past 12 months have increased builder accountability, but the insurance implications of existing defects remain significant.

Insurers require full disclosure of known defects, outstanding rectification works, and capital works programs at renewal. Buildings mid-remediation can still obtain cover, but should work closely with their broker to present a clear remediation timeline and demonstrate proactive management. Failure to disclose known defects is one of the most common causes of claims disputes.

Lithium-Ion Batteries

Lithium-ion battery fires remain a serious and growing concern. Western Australia recorded 94 battery-related fires by August 2025; NSW recorded 25 incidents in the first two months of 2025 alone. Fire services across all states have issued updated safety guidelines, and regulators have introduced new requirements for battery storage and charging management.

For strata schemes, the practical implications are significant. Insurers are scrutinising whether buildings have formal battery management policies covering e-bikes, e-scooters, and EV charging infrastructure. Schemes without such policies, or where charging in common areas is unregulated, are increasingly facing premium loadings or coverage exclusions. This is a rapidly evolving area, and strata committees are encouraged to implement formal policies and document compliance as a priority.

Regulatory Reform: Commission Changes and Strata Law Overhaul

Following the NSW Productivity and Equality Commission's February 2026 report, SCA NSW commenced a voluntary phase-out of insurance commissions from January 2026. Several large strata management firms have already transitioned, replacing commission income with direct administration fees or adjusted management fees. For owners corporations, the practical effect is greater transparency in how their manager is remunerated, owners are encouraged to ask their manager directly. For strata insurance brokers, informed consent to receive commission remains a separate regulatory requirement; this is a transparency measure, not a cost increase.

April 2026 strata law reforms brought stricter conflict of interest disclosure requirements, new regulatory intervention powers in maintenance disputes, consumer protections for owners in levy arrears, higher accountability standards for building managers, and planned mandatory training for strata committee members.

NSW's reforms are catalysing scrutiny nationally. Victoria is the most advanced in response, with a formal review of the Owners Corporations Act 2006 underway examining manager conduct, hidden commissions, and conflicts of interest, legislative changes are anticipated this year. Victoria has also introduced a mandatory 2% defects bond for developers of taller buildings. Queensland has taken a more incremental approach, with 2024 governance reforms and further lot owner protections introduced in April 2026, though it has not yet moved toward a fee-for-service model. The ACT had disclosure requirements predating NSW's changes and is broadly aligned with the transparency direction. Western Australia, South Australia, Tasmania, and the Northern Territory have not yet introduced significant reforms, though pressure from the eastern states is expected to build.

The direction across Australia is consistent: conflicted remuneration in strata management is under sustained regulatory scrutiny, and owners corporations in all states should expect ongoing change.

The strata insurance landscape in 2026 is defined by two converging forces: a softening market creating genuine opportunity for well-managed buildings, and a regulatory environment demanding greater transparency and accountability across the sector.

For owners corporations, the message is consistent throughout. Buildings that are proactively maintained, properly documented, and governed with care are increasingly rewarded, with better insurance terms, broader insurer appetite, and stronger positioning as regulatory standards rise. Those that are not will find the divide harder to close over time.

The reform momentum across NSW and, increasingly, other states signals a sector in transition. Remuneration structures are being scrutinised, governance expectations are rising, and the bar for what constitutes a well-run scheme continues to move. Owners corporations that treat compliance and maintenance as ongoing disciplines rather than reactive obligations will be best placed to navigate what comes next.

If you have questions about how any of the above affects your building's insurance or governance position, please don't hesitate to reach out.